Status Quo of Gold as a Currency

“Fiat money will be a passing fad in the long-term history of money. … Gold is definitely a fiat money hedge.”

-Jim Reid, Deutsche Bank

Key Takeaways

• In 2020, gold proved itself, yet again, as a recession

hedge, a portfolio stabilizer in times of highly volatile

equity markets, and an early inflation hedge.

• After two years of well above average gains of 18.9%

and 24.6% in USD terms and a new all-time high in

August 2020, in 2021 it was time for consolidation in the

gold price.

• Profit-taking, a significantly firmer US dollar, opportunity

costs in the wake of the Bitcoin bull market, and rising

bond yields caused significant headwinds for the gold

price in 2021.

• From 2000 to 2022 gold averaged a 9.3% return. During

this period, gold has outperformed virtually every other

asset class and, above all, every other currency.

• Gold is especially effective as an asset protection tool in

countries where it has a significantly negative

correlation with local stock markets.

• Gold’s long-term upward trend is clearly intact. The

basis for further price increases seems excellent.

Your time is precious, and we won’t beat around the bush: 2021 was

disappointing for gold, especially in view of the sharp rise in inflation

rates.

What were the reasons for this frustrating performance? After record

gains in 2019 and 2020, the gold price had to take a deep breath. After two years of well above average gains of 18.9% and 24.6% in USD terms, and a new all-time high in August 2020, it was time for consolidation. Especially as the impressive 80% rise in the gold price from the August 2018 low to the August 2020 high correctly anticipated the rise in the CPI in 2021

In 2020, gold did exactly what it should do in a diversified portfolio: It served as a reliable hedge against the turmoil in the wake of the Covid-19 pandemic, as a recession hedge, as a portfolio stabilizer in times of highly volatile equity markets, and as an early inflation hedge. In a nutshell, gold has confirmed that it is the Virgil van Dijk of assets. Always on hand when things get really hairy.

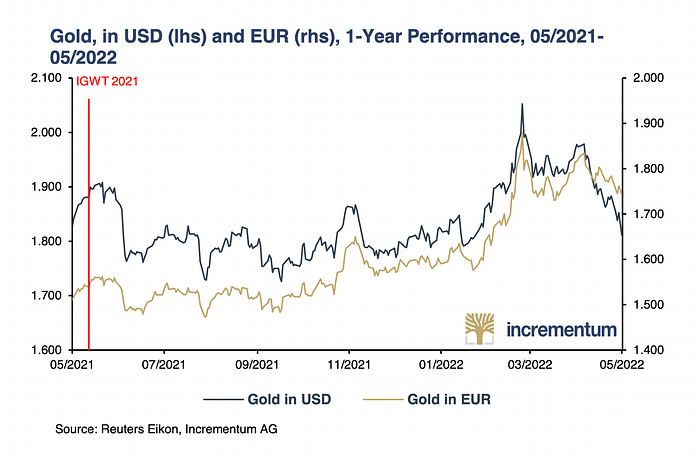

But now back to the present — and the future. Since the start of this year, the tide has turned. Gold started superbly. The all-time high of USD 2,075 from August 7, 2020 was almost reached on March 8, 2022 at USD 2,070. Gold posted its highest quarterly close ever in Q1/2022. In contrast, the US Treasury index posted its worst quarter since the data series began in 1973, losing 5.58%, and the S&P 500 posted its first negative quarterly return since Q1/2020. But from mid-April onwards, a correction set in and the gold price had to pay tribute to the rallying USD as well as the general risk-off sentiment in markets.

At the outset, let’s look at the development of the gold price in the major currencies. The full year 2021 was divergent for gold in the currencies mentioned below. While the gold price in the (former) safe haven currency JPY posted a gain of 7.5%, gold in the Chinese yuan fell by 6.1%. In contrast to the US dollar, the gold price gained 3.6% in euro terms, once again highlighting the glaring weakness of the euro. On average, the gold price lost 0.6%.

As before, the average performance in this secular bull market remains

impressive. The average annual performance from 2000 to 2022 is 9.2%. During this period, gold has outperformed virtually every other asset class and, above all, every other currency — despite significant corrections in the meantime. Since the beginning of 2022 the development has been clearly positive, with an average gain of 5.4%.

Let’s now take a look at the gold price development since the last In

Gold We Trust report in US dollars and euros. Shortly after the publication

of the last report on May 27, 2021, a consolidation phase of several months set in, which only ended at the beginning of 2022. In addition to profit-taking, a significantly firmer US dollar, and opportunity costs in the wake of the Bitcoin bull market, rising bond yields were a major trigger for the emerging headwind.

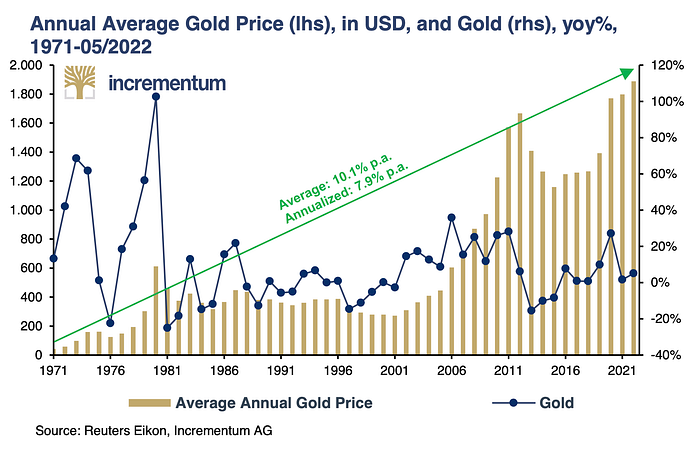

Let’s now flip back even further in the history books. Since the IPO of gold

on August 15, 1971, the average annual growth rate of the gold price in US dollars amounts to 10.1%. The annualized growth rate (CAGR) is 7.9%. In the previous year, gold reached an annual average price of USD 1,799, a new all-time high. Since the beginning of the year, the average gold price has been USD 1,890.

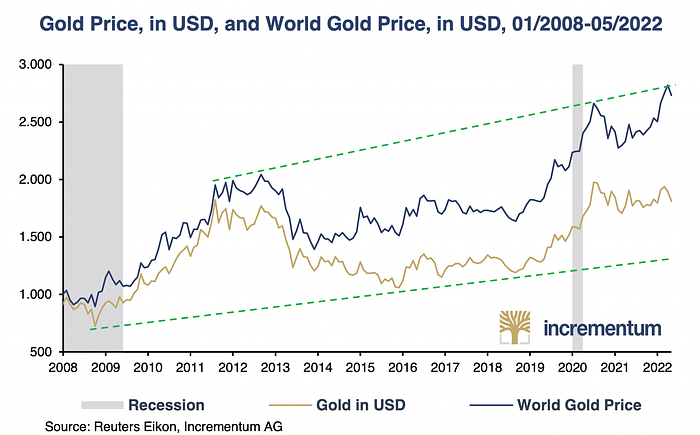

Let us now turn back to the more current “big picture”. The world gold

price, which represents the gold price in the trade-weighted external value of the US dollar, recently reached new all-time highs again. Here, too, it seems that the long-term upward trend is clearly intact.

Why do we actually deal so intensively with the gold price development

in different currencies? For years, we have been surprised that the majority of investors primarily focus on the gold price development in US dollars. In our experience, too few investors ask themselves whether or not they hedge their currency risks.

Thus, gold may rise in US dollars during a crisis but much less in Swiss francs, because the Swiss franc, as a classic safe-haven currency, appreciates against the US dollar and thus retains some of the gains that gold makes in US dollars. For investors from Switzerland, it might therefore be advisable to own gold hedged in Swiss francs in order to also fully benefit from gold’s safe-haven properties. For a euro investor, on the other hand, there is no need to hedge gold investments, in our opinion, as the euro tends to weaken in stress and crisis scenarios.

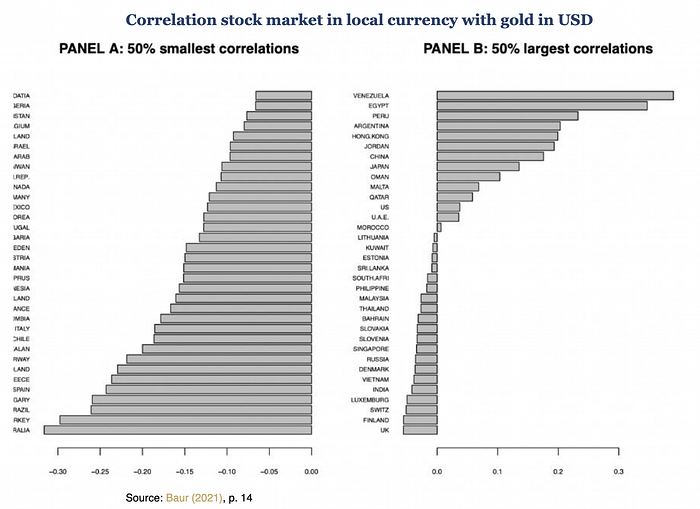

In a study worth reading, Prof. Dirk Baur of the University of Western

Australia analyzed the correlation of gold with the local stock market

in 68 countries. For this purpose, he applied the gold price in US dollars and the gold price in the respective local currency. The table below shows the correlations between the local stock markets and the gold price in local currency.

Note that Venezuela has the highest positive correlation. This is certainly due to hyperinflation in Venezuela, which led to a devaluation of the Venezuelan bolivar and thus a significant appreciation of gold. Stocks rise sharply in times of hyperinflation, not because companies are doing so well, but because there is a flight to real assets.

It can be seen from the chart that for all countries up to Oman and the

US, the protective effect of gold is significantly lower, as gold tends to

have a positive correlation with the local stock markets. In countries from

Oman to Israel or Taiwan, gold has essentially zero correlation with the local equity market, making it quite suitable for diversification. Residents of the countries at the bottom of the list — which include almost all eurozone countries, Sweden, Norway and Australia — should use gold as asset protection due to its significantly negative correlation with the local stock market.

Conclusion

Our assessment of the previous year, according to which gold is in a

new bull market, has proved accurate. Even though the gold price

performed weaker than expected in the past weeks, the broad, long-

term upward trend still seems to be intact.

A look at the Sprott Gold Bullion Sentiment Index2 shows that sentiment had reached an absolute low in March 2021. The indicator had fallen even beyond the second standard deviation in the short term. Since then, the index and the gold price have recovered but are still far from the euphoric levels that prevailed in August 2020, for example. In this respect, the basis for further price increases seems excellent.